What Is a Startup Accelerator? A Founder’s Honest Guide

In this article

- What is a startup accelerator

- How startup accelerators actually work

- Startup accelerator vs incubator vs venture capital

- What you actually give up

- The top startup accelerators in 2026

- Why startup accelerators matter more in the AI era

- Who should apply and who should not

- How to apply

- What happens after demo day

- Frequently asked questions

- Scale your startup with the right engineering model

Y Combinator accepted 0.6% of applicants in its Summer 2025 batch. That is the lowest rate on record, and it tells you most of what you need to know about how a startup accelerator works in 2026. The brand-name programs are now harder to get into than Harvard, Stanford, or MIT. For the other 99 percent, the smarter path is learning how to start a SaaS company without raising venture capital. Accelerators push founders to think about the endgame early, so it helps to read a founder’s guide to startup exits.

I have been a tech founder four times. I cofounded VinSolutions and sold it for around $150 million. I built Stackify and ran it for years. I now run Full Scale and Full Scale Ventures, a startup studio I launched to back the kind of early-stage software companies most accelerators will not touch. I have advised dozens of founders through the application and decision process. I have also watched plenty of them skip accelerators and do fine. An accelerator is optional; building startup software without burning your runway is not.

This guide is what I would tell a founder sitting across from me at a coffee shop, asking whether a startup accelerator is the right move. There are four things to get straight: what an accelerator actually is, how the deal math works, which programs are worth applying to, and what happens the morning after you get the check. That last part is the one nobody on a demo day talks about. If you’re not ready for a full program yet, start by finding a startup mentor who has built what you’re building.

What is a startup accelerator

A startup accelerator is a structured, cohort-based program that gives early-stage companies money, mentorship, and a network in exchange for equity. The cohort runs three to four months. At the end, you pitch investors at a demo day and try to raise a real seed round on the back of the credibility the program just gave you. Long before demo day, that means writing a business plan for your startup tight enough to survive investor questions. An accelerator is just one of several funding resources available to startups, and each carries its own tradeoffs.

Accelerators are sometimes called seed accelerators because they sit at the seed stage of the funding ladder. Founders apply with a small team and at least a working prototype or minimum viable product. The program selects a few dozen companies per batch, gives them all roughly the same deal terms, and runs them through a curriculum focused on customer development, fundraising, and shipping faster.

The model traces back to Y Combinator, which Paul Graham and Jessica Livingston started in 2005. YC has now backed more than 5,600 companies, and the combined portfolio is worth over $600 billion. The list of graduates includes Airbnb, Stripe, Dropbox, DoorDash, and Coinbase. Every accelerator that exists today is either copying that playbook or trying to differentiate against it.

How startup accelerators actually work

The mechanics are simpler than founders tend to assume. There are four parts and they happen in roughly this order.

Application and selection. You submit a written application, often a short video, and references. If the program is interested, you do a 10 to 20 minute interview. The big programs reject 99% of applicants on the written stage and another 70 to 80% at the interview stage. A founder who makes the interview has roughly one in four odds, which is much better than the headline numbers suggest.

Cohort kickoff and the check. Selected companies join a cohort of 20 to 250 startups depending on the program. You sign the standard deal documents and the money hits your bank account. For most programs that is somewhere between $20,000 and $500,000 in exchange for 5% to 10% of your company.

The program itself. Three or four months of weekly office hours, mentor introductions, partner meetings, peer dinners, and a single relentless focus: get to product-market fit and a real metric you can show investors. Some programs run in-person in San Francisco, New York, or Berlin. Others now run fully remote. The best mentors are former founders who built and sold companies in your space, not consultants with a slide deck.

Demo day and the raise. The program ends with a public pitch to a room of investors. You have two to three minutes on stage, a polished deck, and the brand of the accelerator sitting behind you. The goal is not the demo day itself. The goal is the seed round that closes in the four to six weeks after demo day, while every VC in your space still thinks you might be the one they missed.

A good accelerator compresses two years of figuring it out into three months. A bad one charges you 7% of your company for what amounts to a conference badge and a pitch coach. The difference is the network density and the operator quality of the mentors, not the curriculum.

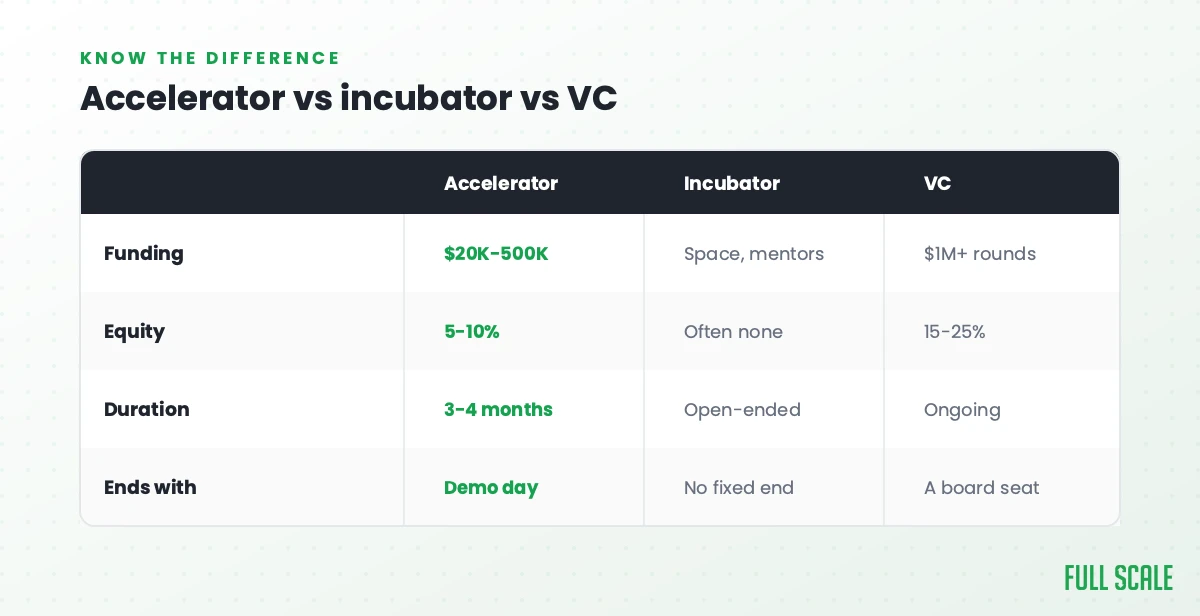

Startup accelerator vs incubator vs venture capital

Accelerators, incubators, and venture capital firms all give startups capital, but they solve different problems at different stages. Founders mix these up constantly, which is how you end up applying for the wrong thing.

| Vehicle | Stage | Duration | Funding | Equity taken | Selection |

|---|---|---|---|---|---|

| Incubator | Idea to early prototype | 1 to 5 years | Usually none, sometimes small grants | 0% to small | Rolling, low bar |

| Accelerator | MVP to early traction | 3 to 4 months | $20K to $500K | 5% to 10% | Cohort-based, very competitive |

| Seed VC | Early revenue, pre-Series A | Indefinite | $500K to $5M | 10% to 25% (round-dependent) | Direct pitch, rolling |

| Series A VC | Product-market fit, repeatable growth | Indefinite | $5M to $25M | 15% to 30% | Direct pitch, rolling |

Use an incubator if you are still figuring out what you are building. Incubators offer space, low-cost resources, and patient mentorship. They rarely take meaningful equity because they are not giving you meaningful capital. Most startups graduate from an incubator with a clearer product idea and a small founding team, not a fundable business. The full breakdown is in our guide to startup incubators.

Use an accelerator if you have a working MVP and want a forcing function. Accelerators are best for founders who already know what they are building and need three months of compressed pressure, mentor access, and a credible story for raising the next round. The trade you are making is 5% to 10% of your company for that compression. If the program is top tier, that trade pays off because the post-accelerator round closes faster and at a higher valuation.

Use direct VC funding if you already have traction and relationships. If you can raise a seed or Series A on your own, you do not need to pay an accelerator 7% for an introduction. The list of top venture capital firms is your starting point. Most VCs are open to a warm intro and a short pitch deck without you having gone through any program at all.

The honest answer for many founders is that none of these is right yet. Bootstrapping for another six months until you have real revenue is often the smartest play. We covered the case for that in our guide to startup bootstrapping.

What you actually give up

Every accelerator pitch focuses on what you get. Founders need to think harder about what you give up, because the equity math is permanent. The same caution applies to trading equity for software development: it can be a smart way to get your product built, but an equity grant is far harder to undo than any cash deal.

Equity. A 7% stake at the seed stage usually dilutes to 4% to 5% by Series A and 2% to 3% by Series C. On a $500 million exit, that 7% is worth around $15 million to $25 million depending on how dilution plays out. That is the price of the accelerator’s check and curriculum. If the program’s network and brand do not unlock more than that in faster fundraising or better customers, you overpaid.

Time. Three months in an accelerator is three months not running your company the way you would run it on your own. The trade is worth it if the program forces you to do things you would have procrastinated on, like talking to 50 customers in a week. It is not worth it if the curriculum is generic and the mentors are not operators in your space.

Control over the narrative. Once you are in a brand-name accelerator, that brand goes on your pitch deck, your hiring page, and your fundraising emails. It opens doors. It also locks you into a path. Founders who graduate from YC find that every subsequent investor compares them against the other YC companies in their batch, whether the comparison is fair or not.

Optionality on your hiring. Most accelerator programs push you to hire fast on the heels of the seed raise. That is sometimes right and sometimes not. Plenty of post-accelerator startups burn through their round in 12 months because they hired five engineers before they had product-market fit. We wrote about how to avoid that in how to reduce startup burn rate.

The top startup accelerators in 2026

There are now hundreds of accelerators globally. Three of them matter for the conversation about whether to apply at all. The rest are useful for specific industries or geographies.

Y Combinator. The standard deal in 2026 is $500,000 total: $125,000 for a fixed 7% equity, plus $375,000 on an uncapped Most Favored Nation SAFE. YC now funds four batches a year of roughly 160 to 170 companies each, runs largely in-person in San Francisco, and has one of the strongest founder networks in tech. The full deal terms are at ycombinator.com/deal. YC-backed companies hit Series A at 45%, versus a 33% industry average, and become unicorns at 4% to 5% versus the 2.5% baseline.

Techstars. Techstars offers $220,000 for 5% equity across a network of city-based and vertical-specific accelerators in Berlin, New York, London, and roughly a dozen other locations. The model is mentor-driven rather than partner-driven, which means the quality varies more by location than it does at YC. If you are building in construction tech, field operations, or another industry where enterprise pilots are the bottleneck, Techstars’s mentor network is hard to beat.

500 Global. Formerly 500 Startups, 500 Global has shifted its center of gravity to international markets. The deal is roughly $150,000 for 6% equity. With over 2,700 companies in 77 countries and $2.4 billion under management, 500 Global is the right choice if your business depends on emerging-market expansion or you want a network that is not concentrated in Silicon Valley.

Beyond the big three, programs like Google for Startups, MassChallenge, and the various corporate accelerators (Disney, Comcast, Microsoft) serve specific niches. The right question is never “which accelerator is best” but “which accelerator has the densest network of operators and investors in my exact space.”

Why startup accelerators matter more in the AI era

A few years ago, the hardest part of starting a software company was building the product. You needed three engineers, a designer, and several months before you had anything to show a prospect.

AI has flipped that. You can now prototype a working product over a weekend with Claude Code, Cursor, or any of half a dozen tools that did not exist 24 months ago. I have called AI “a killer prototyping tool” in my newsletter and I will defend that against anyone who wants to dismiss the tech. For an early-stage founder, it is a real superpower.

The problem is what comes next. Once anyone can build a prototype, building stops being the moat, and the real bottleneck shifts to distribution, sales, and the slow work of talking to 50 customers a week to figure out which ten will actually pay. Those are the muscles most technical founders have never trained, and the ones AI is least useful for.

I wrote a whole newsletter on this called Vibe Coding Entrepreneurs Don’t Scale, and the short version is that building stuff does not make you an entrepreneur, selling does. Most startups die because the founder spent the year building instead of selling.

This is exactly the gap a good accelerator fills. The curriculum is built around forced customer development, weekly metric reviews, and partner intros to investors and early enterprise buyers. The mentors are operators who have done sales and go-to-market themselves. The whole machine is set up to drag a builder out of their editor and onto sales calls. If you are a strong builder who is allergic to selling, an accelerator is the single most effective intervention available to you.

Who should apply and who should not

Accelerators are a great fit for some founders and a waste of time for others. The deciding factor is rarely the strength of the idea. It is the founder’s existing network, stage, and honest self-assessment of whether they can sell.

Apply if you fit one or more of these. You are a first-time founder without warm investor relationships. You are a solo founder and need a built-in support system for the next 18 months. You are a strong technical builder who has never run a sales call and knows you need to learn. You are non-technical and need to find a credible technical team. You are building in a space where the accelerator has 20 mentors who have already done what you are trying to do. You are international and need a US-based credibility wrapper. You have an MVP and at least the start of usage or revenue, even if it is small.

The solo technical founder case is the strongest one I see right now. AI has made it realistic to build an entire MVP alone, but it has also made it harder to stand out once you ship. A good accelerator gives that founder the mentors, the cohort, and the forced sales discipline they would never impose on themselves. That is exactly what someone in that position needs.

Do not apply if any of these are true. You already have a warm intro to three or four seed funds and they are interested. You are revenue-positive and growing 20% month over month without outside capital. You are years past the seed stage and the program would not actually be advising you, it would be branding you. You hate the idea of relocating, doing public pitches, or networking 60 hours a week for three months. Accelerators are not therapy programs and they will not fix a fundamental product or team problem.

The honest test is this: would the program’s mentors and investor network meaningfully change the next 18 months of your business? If yes, apply. If you cannot name three specific mentors whose introductions would matter, the answer is probably no.

How to apply

The application process is similar across the major programs. The bar is high and the rejection rate is brutal, so prepare as if you are pitching a real seed round.

Step one: pick the right program. Look at the last three batches and find the companies most similar to yours. If you cannot find any, your odds are low. Programs select for pattern match.

Step two: write the application like a product. The written application is a screening tool. Be specific, be concrete, and use numbers. “We have 1,200 weekly active users growing 18% week over week” beats “we are gaining traction.” If you have revenue, lead with it. If you do not, lead with whatever real proof you have that customers want the product.

Step three: prepare for the interview. If you make it past the written stage, you get a 10 to 20 minute interview. The interviewers will pick the weakest part of your application and press on it. Have a real answer for “why now,” “why you,” and “why this is a billion-dollar opportunity.” Practice answering in two-sentence bursts, not five-minute monologues.

Step four: have your MVP ready. No accelerator funds a slide deck in 2026. You need a working product, even if it has 20 users and a hideous UI. We have a full guide to MVP development strategy for founders building toward this.

Step five: get strong references. Other founders in the program are the strongest possible reference. If you can get an intro from a recent graduate, take it.

What happens after demo day

This is the part nobody warns you about. The accelerator ends, and you are now responsible for shipping the product, hiring the team, and making the seed round you just raised last 18 to 24 months. That is harder than getting into the program.

A typical post-demo-day startup burns through its seed round in about 14 months. Most of that burn is engineering payroll. If you are paying $180,000 to $250,000 all-in for a senior US developer and you need three of them, you will spend $600,000 to $750,000 a year on engineering alone. That is the entire seed round for many companies.

This is the place where the way you build matters more than the brand on your demo day deck. The founders who survive the post-accelerator stretch usually run a much smaller US team than the conventional advice says they should, and they hire offshore engineers from day one to extend their runway by 18 to 24 months without sacrificing quality.

That is the model we run for accelerator graduates and post-seed startups at Full Scale. Our hire developers in the Philippines and custom software development services pages explain how it works in practice.

The harder part is mindset. Post-seed engineering is not a Jira queue you grind through. It is a series of bets you are making about what users will actually pay for. The whole reason I wrote Product Driven was to give engineering leaders the playbook I wish I had when I was running engineering at VinSolutions.

A startup accelerator can compress a year of learning into three months. It cannot compress the next two years of execution. The execution is the part where most startups die, and the accelerator’s logo on your deck does not save you from that.

Frequently asked questions

How long does a startup accelerator last?

Most accelerator programs run three to four months. Y Combinator’s batch is three months in-person in San Francisco. Techstars runs 13 weeks. A few programs extend to six months, and a handful run year-round with rolling cohorts.

How much equity do startup accelerators take?

The typical accelerator takes 5% to 10% of your company. Y Combinator’s 2026 standard deal is 7% for an initial $125,000, plus $375,000 on an uncapped SAFE. Techstars takes 5% for $220,000. 500 Global takes around 6% for $150,000.

What is the acceptance rate for top startup accelerators?

Y Combinator’s Summer 2025 batch had a 0.6% acceptance rate, the lowest on record. Techstars and 500 Global are also in the 1% to 3% range for their flagship programs. Once you make the interview stage, your odds improve to roughly one in four.

Is a startup accelerator better than venture capital?

They solve different problems. Accelerators are for pre-seed and seed-stage companies that need mentorship, a network, and a credibility wrapper. Venture capital firms invest larger amounts in companies that already have product-market fit. Most successful startups do an accelerator first and then raise from VCs.

Do I need an MVP to apply for a startup accelerator?

Yes, in 2026 you do. Almost no accelerator funds a pitch deck without a working product. Even programs that say they accept idea-stage companies are heavily biased toward teams with at least a prototype, usage data, or a small pilot customer.

What is the difference between an accelerator and an incubator?

Incubators focus on idea-stage and early-prototype companies, run for one to five years, take little or no equity, and offer space and patient mentorship. Accelerators run for three to four months, focus on companies with an MVP, take 5% to 10% equity in exchange for capital, and culminate in a demo day where you pitch investors.

Scale your startup with the right engineering model

Getting into an accelerator is the start of the work, not the end. The 14 months after demo day are when most startups either find product-market fit or run out of money trying. The engineering decisions you make in those months determine which side of the line you end up on.

Full Scale builds and scales engineering teams for accelerator graduates, post-seed startups, and growth-stage companies. We embed senior Filipino engineers directly into your team at a fraction of the US burn rate. That is the difference between burning through your seed round in 14 months and stretching it to 30.

Schedule a free consultation and we will walk through what your engineering team should look like.