What Do Investors Look For in a Startup? The Technical Bets Behind Every Check

In this article

Every startup founder wants to raise money. Almost nobody tells you what the person writing the check is actually buying.

I have been on both sides of that table. I bootstrapped VinSolutions to $35 million in annual revenue with no outside funding, then sold it for $147 million. I founded and sold Stackify. These days I invest in startups myself, I helped fund VinCue as an early backer, and I run a venture studio inside Full Scale called Full Scale Ventures, where we build and bet on products. I have written the deck and I have read the deck. Having sold three companies of my own also shapes how I think about whether to sell at all.

Here is the thing most articles on this topic miss. For a software company, an investment is a technical bet. The investor is not buying your idea. They are buying the team and the machine that turns money into shipped product, and they are betting that machine can keep running without lighting cash on fire.

So when founders ask what investors look for in a startup, the honest answer goes deeper than “a great team and a big market.” Here is what that really means, and what you can do about it before you ever take a meeting.

An investment is a bet on your ability to ship, not your idea

Ideas are cheap. Every investor has heard a hundred versions of yours this quarter.

What they are funding is the gap between your idea and a product customers pay for. That gap is engineering, product judgment, and the discipline to spend money on the right things. A pitch deck is a story about that gap. Due diligence is where they check whether the story is true.

I learned this most clearly from the other chair. On my podcast I interviewed Dave Lambert, founder of Right Side Capital, who has made more than 2,000 startup investments since 2012. His firm runs a quantitative, data-driven process closer to how an underwriter builds a portfolio of loans than how a typical VC falls in love with a founder. When I asked what he scores, the list was not “vision” and “passion.” It was revenue traction, growth rate, average price point, how much capital it took you to get there, your cash burn, and the characteristics of the founding team. What an investor running that kind of volume is really screening for is evidence of product-market fit.

In his words, operational risk and technical competency matter more than founder-market fit. That should tell you where to spend your energy.

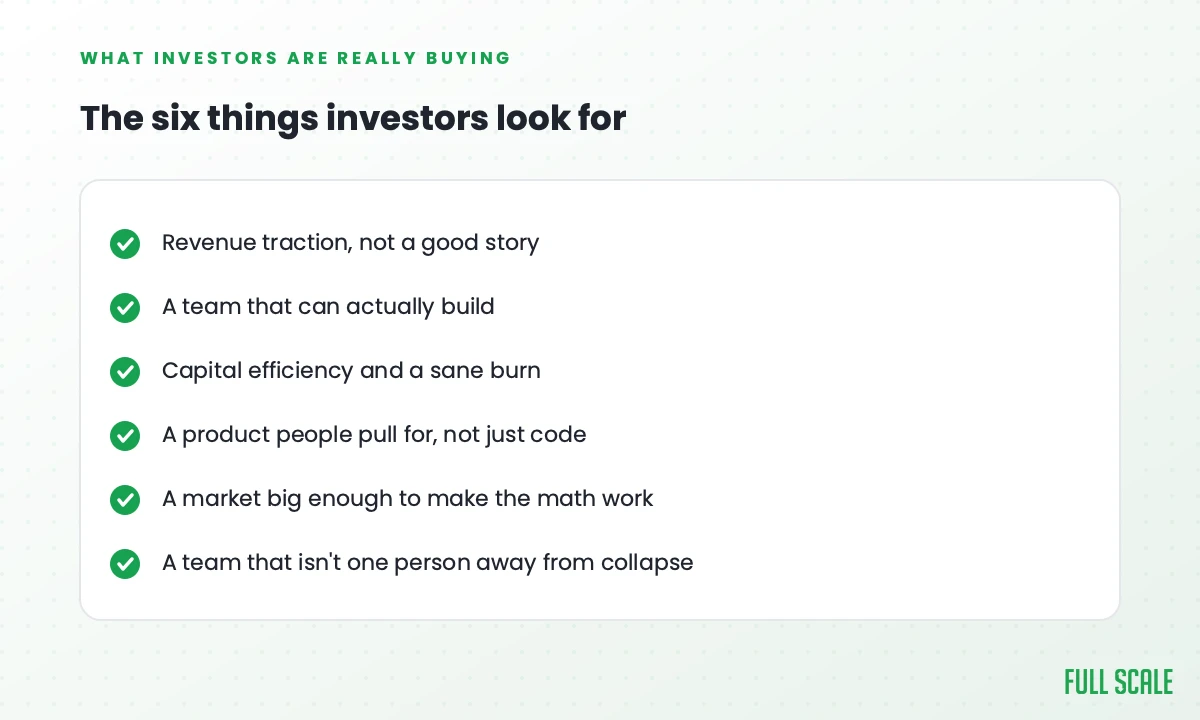

The six things investors actually look for in a startup

The generic checklist you see everywhere is real, but it stops at the surface. Here is the same list with the technical reality investors are testing underneath each item.

1. Revenue traction, not a good story

The fastest way to fail a screen is to show up pre-revenue with a beautiful narrative.

Lambert told me his firm does not invest before there is revenue. The most common range they fund is $5,000 to $30,000 a month. That is not a huge number. It is proof that a real human paid you real money for the thing you built, which is the only evidence that your engineering produced something the market wanted.

Build the smallest version that someone will pay for, then show the curve. Traction beats projections every time.

2. A founding team that can actually build the thing

Most software startups that get funded have a technical founder for a reason.

Investors are betting that your team can ship faster and cheaper than the competition, adapt when the plan changes, and not need a rescue six months in. They are reading the team the way I read a team when I invest: can these people turn a dollar into working software, or are they going to need to hire their way out of every problem?

This is also where founders sabotage themselves before they start. Nothing will kill a startup faster than entry level software developers. Padding your headcount with cheap, junior engineers to look bigger is the opposite of what a sharp investor wants to see. They want a small team that punches above its weight, because that is what survives a lean year.

3. Capital efficiency and a burn rate that makes sense

Notice two of the things Lambert scores: how much capital it took to get here, and your cash burn.

Investors are not just asking how big you can get. They are asking how little you can waste on the way. A team that reached $20,000 in monthly revenue on a shoestring is far more fundable than one that burned a million dollars to get to the same place. Efficiency is a signal that you make good decisions under constraint, and that their money will go further than it would somewhere else.

This is the single biggest lever a technical founder controls, and it runs straight through your engineering payroll. The median US software developer earns $133,080, and a senior engineer in a major market runs well past $150,000 in base pay before you add benefits, taxes, and equity. Five of them is most of a seed round before you have shipped anything. How you staff that team is a fundraising decision, not just a hiring one.

4. A product people pull for, not just clean code

Here is a contrarian one that investors understand and a lot of engineers resist.

Customers don’t buy cool code. They buy cool products. The teams that win are the ones connected to what users actually need, not the ones with the prettiest architecture. This is the whole argument of my book, Product Driven: most of what software teams ship never matters to a customer, and the rare team that ships the things that do matter is the one worth backing.

When an investor probes your roadmap, they are checking for product judgment. Can you tell the difference between a feature that closes deals and a feature that just feels good to build? That judgment is worth more than raw coding horsepower. As I like to put it, the expert in the problem will always beat the expert in the code.

5. A market big enough to make the math work

This is table stakes, and the generic articles cover it well, so I will keep it short.

Investors need a believable path to a return, which means the market has to be large enough that your slice of it pays back the whole fund. Be honest about size. A tight, real $50 million market you can win beats a fantasy $50 billion market you have no wedge into. If you want the full treatment on market sizing and the funding ladder, that is a finance topic with plenty of good writing already out there.

6. A team that isn’t one person away from collapse

The last thing investors look for is the one founders never put on a slide: key-person risk.

If all the knowledge of how your system works lives in one founder’s head, that is a problem they will price in or pass on. The same is true if your codebase is a black box only one contractor understands. They are asking whether the company survives if you get hit by a bus, and whether the next ten engineers can understand and extend what you built. Hold onto that one, because it is exactly what a technical reviewer goes looking for.

What technical due diligence actually checks

Once a deal gets serious, especially at a real Series A, the investor brings in someone technical to look under the hood. Founders are rarely ready for this because no one explains what it is. This step used to be optional, and now it usually is not, partly because so many products that demo beautifully turn out to be held together by AI-generated code nobody on the team can explain. A due-diligence review is how the investor finds out before they wire the money.

It is not a code-quality contest. It is a risk assessment. A technical reviewer is trying to answer a handful of plain questions:

- Can this team keep shipping, or is the codebase held together by one person and a prayer?

- Will it survive the next order of magnitude of growth without a full rewrite?

- Is there an obvious security or data landmine, the kind that becomes a breach later?

- Does the spend match the output, or is the burn paying for a team that out-architected the problem?

Then there is the paperwork side that kills more deals than bad code does. The fastest way to lose a check is to not clearly own your own code. If a founder or a contractor never signed their work over to the company, the intellectual property is in question, and a sharp investor walks. That is the single most common deal-breaker I see, ahead of security gaps and undocumented architecture. If you used offshore or contract help to build the product, get the IP assignment in writing before anyone looks.

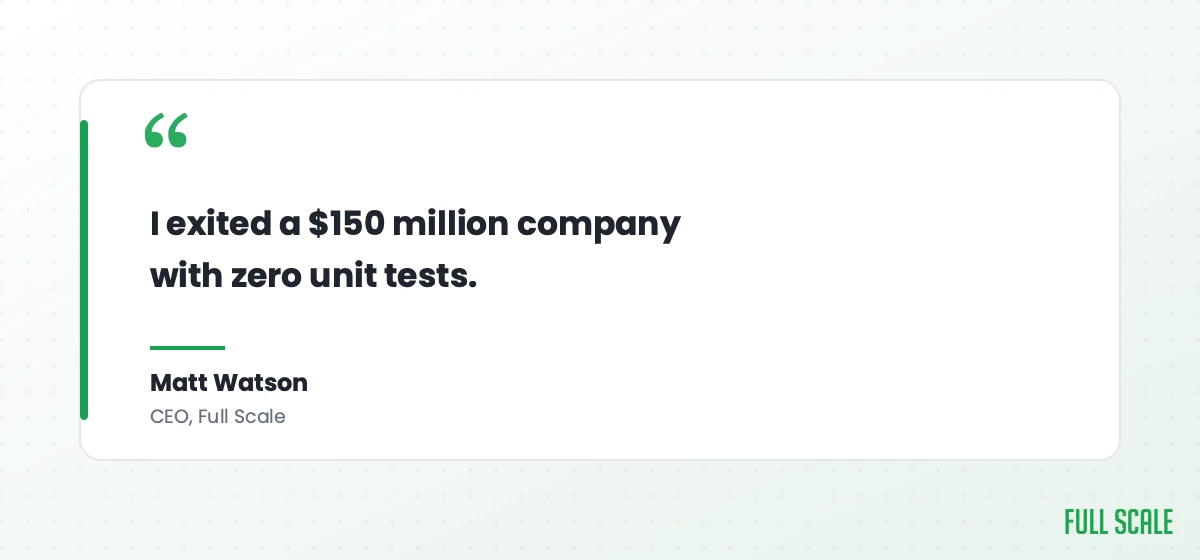

Here is where I push back on the fear most founders carry into this. I exited a $150 million company with zero unit tests. I am not telling you to skip tests. I am telling you that a smart reviewer is not grading you against an imaginary perfect codebase. The non-negotiables are clear ownership of the code, no glaring security holes, and a system the next engineer can actually understand. The things founders panic about, like test coverage percentages and whether you used microservices, barely move the needle. A pristine, over-engineered system with no traction fails diligence worse than a boring, slightly messy one that ships and sells.

Which is exactly the point: keep it simple and boring until you can’t. I scaled VinSolutions to $35 million in revenue on essentially one big database server and a couple of read replicas, before microservices were the fashionable answer. Exotic architecture is not a fundability signal. A product that works, code you clearly own, and a team that can maintain it are.

The engineering-money moves that make you fundable

A founder controls a handful of engineering-money decisions, and those decisions are most of what an investor is judging. You cannot move the market or the macro. You can control these.

Staff lean, and stretch your runway with augmentation. The fastest way to wreck your capital efficiency is to over-hire senior US engineers before you have product-market fit. A more fundable pattern is a small core team augmented with senior offshore engineers who work as part of your team, not a faceless vendor. A senior US hire can run $200,000 or more all-in; a senior engineer through Full Scale staff augmentation bills around $35 an hour. Across a year of runway that gap buys you months, and months are what investors like Lambert are scoring when they look at your burn.

There is an honest tension to name here, because it is the same risk I told you investors price in. An offshore-heavy team is exactly where a technical reviewer goes hunting for key-person and black-box problems: who owns the code, can anyone besides one contractor explain it, does the knowledge live with the company or walk out the door. Augmentation passes that test when the engineers are integrated into your team, the IP is assigned to you in writing, and the work is documented. It fails when you hand a spec to a faceless vendor and hope. That difference is everything, and it is the line between real augmentation and the cheapshoring trap that comes next.

Do not chase the cheapest developer. Lower burn is the goal, but there is a trap here. Hiring the cheapest body you can find, what I call cheapshoring, usually costs more once you count the rework and the missed deadlines. Capital efficiency means getting more output per dollar, not paying the smallest possible rate for the least output.

Treat technical debt as a line item. Debt you take on knowingly to ship faster is fine. Debt that piles up because nobody is steering will surface in due diligence and slow every future release. The real cost of technical debt is the velocity you lose later, and investors can feel that in your release cadence.

Remember that you don’t need rockstar developers. You need rockstar requirements. The teams that ship the right things cheaply are the ones with clear product direction, not the ones with the most expensive resumes.

If you would rather not raise at all, that is a legitimate path too. I bootstrapped a company to a nine-figure exit without taking a dollar, and there is a real argument for staying bootstrapped if your model allows it. Raising is a tool, not a trophy.

The check follows the machine

Investors are not buying your pitch. They are buying a team that turns money into product customers pay for, and they are betting it can keep doing that without burning through their capital.

Everything they look for, traction, the team, the burn, the product judgment, the technical risk, comes back to that one bet. Build the machine that wins the bet, and the funding is a lot easier to find.

Keep it simple, spend like the money is yours, and ship things that matter.

Frequently asked questions

What do investors look for in a startup first?

Revenue traction. For a software startup, the first screen is usually evidence that real customers pay for what you built, even at a small scale. Investors like Right Side Capital often will not look at a company until it has revenue, commonly in the $5,000 to $30,000 a month range. A working product with paying users beats projections and a polished deck every time.

Why do most startups fail to raise or survive?

The most common killer is running out of cash, which usually traces back to building something the market did not want or burning money faster than the business could support. About half of new businesses do not make it to five years, per US Bureau of Labor Statistics survival data. For startups specifically, capital efficiency and real demand are what separate the ones that get funded from the ones that stall. Investors are only one of the startup funding sources worth considering, depending on what you need to build.

Do investors care about my code quality?

Yes, but not the way founders fear. In technical due diligence a reviewer checks whether your team can keep shipping, whether the system survives growth, and whether there are obvious security or data risks. They are not grading you against a perfect codebase. What sinks a deal is unclear ownership of the code, a security hole, or a system only one person understands, not a missing test suite.

How can a startup lower its burn rate without slowing down?

Staff a small, senior core team and augment it with experienced offshore engineers instead of over-hiring expensive in-house headcount before product-market fit. This lowers monthly burn and extends runway, both of which improve how investors score your capital efficiency. Avoid hiring the cheapest developers you can find, since rework usually erases the savings.

Thinking about a raise and worried your burn or your engineering team won’t hold up to scrutiny? Full Scale helps founders build lean, senior engineering teams that stretch runway and show investors a capital-efficient machine. Schedule a call and let’s talk through your team.